Nonprofit Financial Management: Overview + Best Practices

Thursday, April 2, 2026 by Jon Osterburg

As a nonprofit professional, your primary focus is advancing your organization's mission, so most of your activities likely revolve around running community programs and fundraising. But as you work on the many critical initiatives you have planned for these areas, financial management tasks sometimes take a backseat.

However, effective financial management is essential to ensure your nonprofit has the necessary resources to pursue its mission. To help you get started, this guide will cover the basics of nonprofit financial management, including:

- Nonprofit Financial Management FAQ

- Financial Policies: The Foundation of Effective Management

- Key Nonprofit Financial Documents

- Additional Nonprofit Financial Management Best Practices

Before we dive into actionable strategies for nonprofit financial management, let's make sure we're all on the same page about what this term means and why it matters for your organization.

Level up your nonprofit's financial management by partnering with the experts at Jitasa.

Request a QuoteNonprofit Financial Management: Frequently Asked Questions

What is nonprofit financial management?

Nonprofit financial management is the strategic process of planning and monitoring a tax-exempt organization's financial resources. Its overarching goal is to achieve sustainable financial health for your organization and maintain accountability.

Activities like bookkeeping, accounting, and financial planning fall under the umbrella of financial management. However, the goals, strategies, and procedures developed through these activities affect your entire nonprofit's day-to-day operations.

Why is nonprofit financial management important?

While for-profit organizations manage their finances with the goal of maximizing profits, nonprofits like yours focus on using resources to maximize community impact. Here are just a few of the ways financial management can benefit your organization:

- Effective stewardship of the various monetary and in-kind contributions you bring in through fundraising.

- Increased transparency with supporters, which builds trust that leads to long-term engagement.

- Improved risk management abilities through proactive prevention and mitigation.

- Compliance with various regulations, such as IRS legal guidelines for tax-exempt organizations and the Generally Accepted Accounting Principles (GAAP).

- Data-driven decision-making, especially regarding growth preparation.

Think of financial management as the bridge between fundraising and service delivery. To make a difference in its community, your nonprofit not only needs to bring in sufficient funds but also properly allocate that revenue across its programs and operations. Then, your impact combined with transparency about your financial management practices, will lead more supporters to contribute to your fundraising efforts.

Who is responsible for effective nonprofit financial management?

Naturally, your nonprofit's finance team is primarily responsible for effectively managing your organization's finances. The members of this team typically include your:

- Treasurer. As a member of your organization's board of directors, your treasurer provides financial oversight for your nonprofit. Besides approving key documents like your operating budget and annual tax return (more on these later!), your treasurer also regularly reports your organization's financial situation to the rest of the board.

- Chief financial officer (CFO). Your CFO is responsible for financial strategy activities like budget creation and cash flow forecasting. They work closely with the rest of your leadership team and can either be a full-time employee or hired on a part-time (fractional) basis.

- Bookkeeper. This team member (or volunteer for very small organizations) takes care of your nonprofit's daily financial needs, such as inputting transaction data, writing checks, and managing invoices. The keyword to associate with this position is recordkeeping.

- Accountant. This professional is responsible for financial analysis and reporting tasks like reconciling bank records, creating financial statements, and filing tax forms. Depending on your organization's needs and budget, you could hire an accountant in-house or leverage outsourced accounting services (more on this later, too!).

Although every nonprofit needs a treasurer, some organizations structure the rest of their financial teams a bit differently by having a controller lead the charge and manage other professionals in various positions. No matter which model your nonprofit uses, the important things to remember are 1) that you should have multiple financial professionals to ensure accuracy and adequate staffing, and 2) that everyone at your organization needs to understand how financial management applies to their specific roles so they can support your finance team.

Financial Policies: The Foundation of Effective Management

To lay the groundwork for effective financial management, your nonprofit needs to develop a set of fiscal policies and procedures that govern your team's day-to-day use of funds. Compile all of the policies you develop into a handbook, and share this resource with your staff and board members so they can reference it whenever necessary.

While there are a plethora of policies and procedures your nonprofit could enact, we'll cover a few of the most important in the following sections.

Gift Acceptance Policy

Imagine your nonprofit is planning its annual silent auction fundraiser. To keep the event's upfront costs as low as possible, you solicit in-kind donations of auction prizes from individual donors and local businesses, and you receive many useful items through this channel.

Then one day, a supporter brings in an assortment of scented lotions, facial masks, and other at-home spa supplies. You think this will make a great gift basket—until you realize that several items are missing their safety seals. These contributions could be dangerous to sell to an auction participant, but the donor obviously meant well. How should you respond in this situation?

Gift acceptance policies help prevent these issues from occurring in the first place and provide guidance for dealing with them when they do. These guidelines should include:

- The types of gifts (both in-kind and monetary) your organization can and can't accept

- The circumstances or conditions under which you'll accept various donations

- The procedures for recording different kinds of gifts

By showing the misguided supporter in our example the official policy that states that donations of personal care items need to be unopened, your team can politely decline the gift without seeming ungrateful. Additionally, if you explain the policy in your supporter communications, you can encourage even more eligible contributions of various types—money, physical goods, pro bono services, and immaterial assets like real estate and stock donations.

Use our customizable template to create your nonprofit's gift acceptance policy.

Download for FreeConflict of Interest Policy

Conflicts of interest occur when nonprofit leaders, board members, or other key players have professional or personal interests that may oppose their duty to act in your organization's best interest. For example, if a board member owns a software company and your nonprofit is considering purchasing that type of software, that would likely be considered a conflict of interest.

To effectively navigate these situations, include the following in your organization's conflict of interest policy:

- Your nonprofit's definition of a conflict of interest

- The proper timeline and method for disclosing conflicts

- The next steps to take after a conflict of interest is disclosed or discovered

In the example situation, your organization's conflict of interest policy may require that the board choose a different solution or that the company owner abstain from voting. Besides removing bias from financial decision-making, this policy can protect your nonprofit's reputation by ensuring conflicts are managed proactively.

Expense Reimbursement Policy

Your nonprofit should have a bank account with funding set aside for each of your expenses. However, there may still be times when your staff members or volunteers spend their personal money on behalf of your cause, whether they're buying supplies for an event or paying the registration fee for an industry conference. When this occurs, they may be able to be reimbursed—if you have a policy that allows you to provide expense reimbursements!

In your expense reimbursement policy, include information about:

- The types of expenses that can be reimbursed

- The information that should be submitted in reimbursement requests (items purchased, cost, reason for purchase, etc.)

- The staff member(s) responsible for providing the reimbursement

- The procedure for recording reimbursements

Make sure to include deadlines in your policy, both for submitting reimbursement requests and for paying out reimbursed funds. Many organizations use a 30- or 60-day window for each of these deadlines.

Staff Compensation Policy

A common myth about the nonprofit sector is that employees don't make living wages—and they shouldn't so that the organization can put as much funding as possible toward its mission. While some nonprofit staff members are willing to take a pay cut to work for a cause that matters to them, they deserve to be compensated fairly for their efforts. Plus, by providing fair and competitive compensation, you can boost employee retention and actually save money in the long run!

To make this happen for your organization, create a staff compensation policy that outlines:

- Your nonprofit's compensation structure and elements

- The procedure for approving compensation for new and existing roles

- The timeline for reviewing and raising compensation rates

As you create this policy, make sure to consider all aspects of your employees' compensation. This includes not only direct compensation like salaries and bonuses, but also indirect compensation like healthcare and retirement benefits, paid time off, and professional development opportunities.

Key Nonprofit Financial Documents

In addition to your financial policy handbook, there are several resources you'll need to effectively plan and report your nonprofit's finances. Let's review four essential categories of nonprofit financial documents in more detail.

Budgets

The most important aspect of your nonprofit's financial planning processes is budgeting, in which your team (typically led by your CFO) creates documents that outline your organization's revenue and expenses for a specific time period and/or activity.

The most common type of nonprofit budget is an annual operating budget, which covers all of your organization's financial activities for a given year. It usually breaks down your projected revenue by source and predicted expenses based on their role in fulfilling your nonprofit's mission.

However, there are several other types of budgets your organization might create, including:

- Capital budgets, which cover long-term, large-scale projects like capital campaigns

- Program budgets, which help your organization plan specific community outreach initiatives or services

- Grant proposal budgets, which you'll submit along with grant applications to show grantmakers how you plan to use their funding if you secure it

- Fundraising campaign budgets, which detail the expenses associated with events or other significant fundraisers and the revenue you'll use to cover them

No matter what type of budget you need, make sure it includes well-defined goals and realistic metrics to effectively guide your nonprofit's spending and revenue generation efforts.

Chart of Accounts

Your nonprofit's chart of accounts (COA) serves as its financial directory. It's a table-style list of all of your organization's financial accounts and records, making it the backbone of all accounting procedures and a key reference for anyone needing to reference specific financial data.

Most nonprofits divide their COA into five categories and use the following numbering system for reference:

- Assets (account numbers beginning with 1000): Everything your nonprofit owns, such as cash, property, and accounts receivable.

- Liabilities (account numbers beginning with 2000): Everything your nonprofit owes, such as debt, deferred revenue, and accounts payable.

- Net assets (account numbers beginning with 3000): The total amount your nonprofit is worth, calculated by subtracting your liabilities from your assets. Most organizations also separate unrestricted net assets from net assets with donor restrictions.

- Revenue (account numbers beginning with 4000-6000): All of the income your nonprofit brings in, including both monetary and non-monetary funding sources.

- Expenses (account numbers beginning with 7000-9000): All of the costs your nonprofit incurs, whether they're related to your programs or operations.

This system of categorization is based on the Unified Chart of Accounts (UCOA), a standardized chart of accounts that aligns with nonprofit reporting requirements. However, many organizations find the complete UCOA too complicated for their needs, so consider it a starting point and customize your COA to include only the accounts your nonprofit regularly uses.

Financial Statements

One of the main purposes of your nonprofit's chart of accounts is to inform its financial statements—essential reports that your organization should compile each year. Financial statements organize and summarize your nonprofit's financial data so you can draw actionable conclusions from it.

The four core nonprofit financial statements include the:

- Statement of activities. As the nonprofit parallel to the for-profit income statement, this report is integral to the budgeting process. It breaks down your organization's revenue, expenses, and net assets so you can compare your actual numbers for the year to the projections in your last budget and make more accurate predictions for next year.

- Statement of financial position. Also known as a balance sheet, this statement lays out your nonprofit's assets, liabilities, and net assets. This provides a snapshot of your organization's financial health and is helpful in planning for growth.

- Statement of cash flows. This report shows how cash moves in and out of your organization through operating, investing, and financing activities. It's usually pulled monthly rather than annually so that your team can use it to keep your spending and fundraising on track throughout the year.

- Statement of functional expenses. The one financial statement unique to nonprofits, this report organizes your expenditures based on whether they're used for programs, administrative activities, or fundraising so you can see how your spending furthers your mission.

In addition to using financial statements for internal decision-making, many nonprofits attach them as appendices to their annual reports to promote transparency with supporters and stakeholders who may want to learn more about the organization's financial situation.

Tax Forms

The main purpose of your financial statements is to inform your nonprofit's annual tax returns. When your organization was established, its founders filed Form 1023 with the IRS to obtain 501(c)(3) status, meaning your nonprofit is exempt from federal income tax. To prove that your organization still deserves this status, you have to file a tax return via Form 990 every year.

There are four versions of Form 990 that your organization could file based on its size and designation:

- Form 990-N: Small nonprofits with less than $50,000 in annual gross receipts are eligible to file this eight-question digital form.

- Form 990-EZ: If your organization's annual gross receipts total less than $200,000 and your total assets are worth less than $500,000, you can complete this four-page form.

- Form 990: Your nonprofit is required to file the full 12-page return if its annual gross receipts total $200,000 or more or your total assets are worth $500,000 or more.

- Form 990-PF: All private foundations have to complete this 13-page form, regardless of gross receipts or total assets.

To figure out which Form 990 variation your organization needs to file, take the quick quiz below!

Which Form 990 Version Should Your Nonprofit File?

Your organization should likely file:

Jitasa's nonprofit tax team has completed more than 5,000 Form 990 filings—and they can help with your organization's, too!

Request a QuoteUnless your organization requests an official extension using Form 8868, the deadline for filing any type of Form 990 is the 15th day of the fifth month after your nonprofit's fiscal year ends. If your organization's fiscal year follows the calendar year, your Form 990 is due on May 15. Filing late can incur penalties, so plan ahead to complete your return on time.

Additionally, since your nonprofit is an employer, you'll need to file tax forms for all of your employees to help them pay their income taxes. Complete a Form W-2 for each staff member on your organization's payroll and a Form 1099 for any contractors you work with by January 31 of each year (regardless of when your nonprofit's fiscal year ends).

Additional Financial Management Best Practices

Effective nonprofit financial management is more than just implementing the right policies and creating compliant reports. It also includes the decisions you make to put your organization on a path to sustainable growth. Here are five best practices to help you do just that!

1. Diversify Your Revenue Streams

You've likely heard that you shouldn't put all of your eggs in one basket when it comes to nonprofit revenue generation to ensure sustainability. If a funding source falls short of its goal or expenses are higher than expected, it's easier to recover if your nonprofit has a diversified revenue model.

Here are the major categories of nonprofit revenue and a few types of funding that fall under each one:

- Individual donations: Small, mid-level, and major gifts; event revenue; in-kind contributions

- Corporate philanthropy: Sponsorships, matching gifts, volunteer grants

- Earned income: Membership dues, merchandise sales, fees for services

- Investments: Endowments, stocks, bonds, mutual funds

- Grants: Federal, state, and local government grants; public, private, and family foundation grants

Choose several sources from this list to incorporate into your strategy, taking into account your team's capacity, your organization's connections, and your supporters' giving preferences. Then, ensure all of your revenue is reinvested into your nonprofit, whether through expenditures that support your mission and operations or deposits into your organization's reserve funds.

2. Maintain the Right Expense Ratio

In your nonprofit's operating budget, statement of functional expenses, and Form 990, your expenses will be broken down into the following three categories based on how that spending furthers your mission:

- Program costs: Expenses directly related to making a difference in the community, which vary widely by organization (for example, a nonprofit that provides free after-school tutoring would put the cost of students' books and school supplies under its program expenses).

- Administrative costs: Expenses that are necessary to operate your organization, such as staff compensation, utility bills, and office equipment purchases.

- Fundraising costs: Expenses associated with launching fundraising campaigns, including event planning, marketing, and fundraising software fees.

You might also have heard the term "overhead expenses," which refers to your nonprofit's administrative and fundraising costs combined. Overhead isn't inherently bad—some of these expenses are essential for your organization to thrive. However, your goal should be to put as much of your funding toward your mission as possible.

The widely accepted rule of the past was that nonprofits' expenses should consist of 65% program costs and 35% overhead, but the exact breakdown will look different for every organization. Treat this "rule" as a guideline to find ways to reduce overhead costs within reason and allocate your resources wisely toward mission-related activities.

3. Focus on Donor Retention

As of the end of 2024, the average year-over-year donor retention rate in the nonprofit sector was just under 35%. This means that if your organization received contributions from 100 individuals last year, only 35 of them would give again this year.

However, retaining donors is significantly more cost-effective than acquiring new ones. On average, nonprofits spend $1.50 per dollar raised to acquire a new donor, but only $0.20 per dollar raised to retain an existing donor. Plus, donor retention allows you to build stronger relationships with supporters, which often leads them to increase their contributions or engage with your nonprofit in other ways.

There will be times when your organization will need to put more effort into donor acquisition, especially if you're planning for growth. However, prioritizing retention day-to-day will help you manage your nonprofit's finances more effectively.

4. Use Dedicated Accounting Software

Across all areas of your nonprofit's operations, it's important to maintain consistency in data entry and practice good data hygiene. However, proper management of information matters even more when it comes to your organization's finances—not only do you need organized, accurate data to make informed decisions, but it's also critical for compliance.

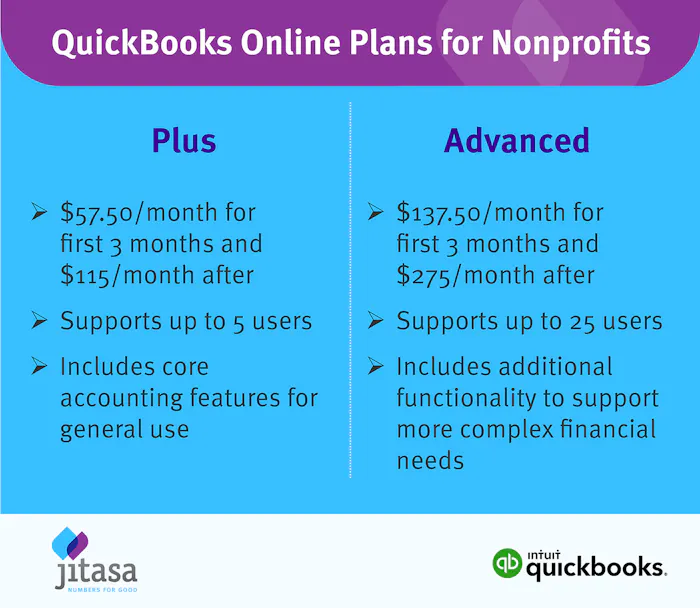

The best way to manage financial data is to invest in a dedicated accounting platform. Jitasa's team are experts in the most common accounting solutions for nonprofits. One that we've found works for many is QuickBooks Online since it's cloud-based (allowing for seamless, secure collaboration) and relatively simple to customize to your organization's needs.

QuickBooks Online has two plans available for nonprofits: Plus and Advanced. The primary differences between these plans are functionality and user permissions. If your organization is just starting out with accounting software, the Plus plan will likely meet your needs. However, if you need access for more than five users (the limit on the Plus plan) or more extensive features like batch invoices or dedicated employee expense records, it's worth it to upgrade to the Advanced plan.

5. Outsource Your Financial Management Needs

Very large nonprofits often hire financial professionals in-house because their needs are complex enough for full-time staff to manage them. However, many small, mid-sized, and growing organizations don't have the budget or workload necessary to justify filling all necessary roles internally. Instead, outsourced financial management services provide access to all of the expertise these nonprofits need at a fraction of the cost.

At Jitasa, we offer a full slate of outsourced financial management services, including:

- Bookkeeping and accounting services that are flat-rate, personalized, and scalable.

- Tax services—we've completed more than 5,000 nonprofit tax filings to date!

- Fractional CFO services through the Jitasa Strategic Advisory Team (J-SAT).

- Controller services focused on compliance and operational improvement.

Plus, Jitasa works exclusively with nonprofits, so we understand your organization's unique needs. If you have a financial situation that you don't know how to navigate, chances are we've seen something similar before and can use our experience to help you solve problems and achieve your goals.

Effective nonprofit financial management allows your organization to achieve the health and sustainability necessary to pursue your mission and take on additional growth opportunities. Use the advice in this guide to get started, and don't hesitate to reach out to nonprofit financial professionals (like our team at Jitasa) about any questions or needs that may arise.

For more information on nonprofit financial management, check out these resources:

- What Is a Nonprofit Audit? Ultimate Guide + Checklist. Another action your nonprofit can take to more effectively manage its finances is to conduct independent audits—learn more about these processes in this guide.

- Grant Management: How to Secure and Track Nonprofit Funding. Dive deeper into the process of identifying, applying for, and utilizing grants as it relates to your overall financial management strategy.

- Church Accounting: Ultimate Guide + Best Practices to Know. Explore the ins and outs of church financial management, which is somewhat similar to other tax-exempt organizations but also includes some unique considerations.

Effectively manage your nonprofit's finances with Jitasa's affordable, scalable bookkeeping and accounting services.

Request a Quote