Nonprofit Revenue Recognition: What It Is & Why It Matters

Thursday, March 12, 2026 by Jon Osterburg

To increase your nonprofit's financial stability, you need to bring in funding from various sources, such as individual donations, corporate contributions, and grants. However, the more diverse your organization's revenue streams are, the more complicated it becomes to record and report your funding.

This is why proper revenue recognition is critical for your nonprofit. In this guide, you'll learn all you need to know about the process of nonprofit revenue recognition, including:

- Nonprofit Revenue Recognition FAQ

- Revenue Recognition Key Terms for Nonprofits

- Common Revenue Recognition Pain Points (& Their Solutions!)

When you consistently recognize funding, you can ensure compliance with legal requirements and streamline your financial management activities for better results. Let's get started by breaking down what exactly nonprofit revenue recognition is and addressing other frequently asked questions on the subject.

Ensure your nonprofit recognizes its revenue properly with expert help from Jitasa.

Request a QuoteNonprofit Revenue Recognition: Frequently Asked Questions

What is nonprofit revenue recognition?

Nonprofit revenue recognition refers to the procedures charitable organizations use to record and report the funding they receive. It's essential for financial transparency, accountability, and effective resource management.

Since your reports should always line up with your records, revenue recognition principles apply to both internal recordkeeping and external income reporting on your nonprofit's financial statements, annual tax return, and other key accounting documents.

Why is nonprofit revenue recognition important?

Correctly recognizing your organization's revenue ensures that you comply with various regulations relating to nonprofit finances. Some of these include:

- Financial Accounting Standards Board (FASB) rules. The FASB is the private-entity governing body of accounting for both nonprofit and for-profit organizations in the U.S. Its Accounting Standards Codification (ASC) 606 outlines how all organizations that enter into financial contracts should report their revenue.

- Generally Accepted Accounting Principles (GAAP). These agreed-upon accounting standards promote accountability in financial management across all sectors through standardized practices, such as how to recognize revenue.

- IRS tax reporting requirements. When your nonprofit files its annual tax return via IRS Form 990, the way you've recognized revenue throughout the year will affect how you complete your report, which needs to be as accurate as possible to ensure your organization can remain tax-exempt and in good standing with the government.

Beyond compliance, an effective revenue recognition system streamlines financial activities at your nonprofit. Your internal records will be better organized, and it'll be easier to prioritize financial transparency with stakeholders when you know how your revenue has been recognized.

How can my nonprofit standardize its revenue recognition practices?

Creating a revenue (or income) recognition policy is the best way to standardize revenue recognition processes at your nonprofit. In this document, make sure to outline:

- The types of revenue covered by the policy.

- How each of these types of revenue is classified (i.e., contribution vs. exchange transaction—more on these terms later!).

- When and how each revenue classification should be recorded.

- How conditions and restrictions affect revenue recognition.

- Comprehensive revenue reporting procedures.

- Internal controls and other oversight measures to ensure the policy is followed.

- Guidelines and a schedule for reviewing and updating the policy over time.

Once you've developed a revenue recognition policy, add it to your nonprofit's financial policy handbook to ensure all team members can reference it as needed.

Use our customizable template to create your nonprofit's income recognition policy.

Download for FreeRevenue Recognition Key Terms

When you're getting started with nonprofit revenue recognition, it's often helpful to frame the process around its key terms. While you may have some familiarity with these concepts from requesting and processing donations for your organization, we'll review the nonprofit accounting terminology and discuss the applications of each in more detail.

Contribution Transactions

Any time money moves in or out of your organization in such a way that it changes hands from one party to another, it's known as a transaction. Contribution transactions occur when your nonprofit obtains funds without the contributing individual or organization directly receiving anything in return.

Examples of contribution transactions include:

- Most individual monetary contributions (small, mid-level, major, and planned).

- Some types of corporate giving, such as matching gifts, volunteer grants, and internal employee fundraising campaigns.

- Most in-kind donations of goods, services, and non-cash assets like stocks or real estate.

- Government and foundation grants.

In most cases, your nonprofit should recognize contribution transactions as soon as you know the full amount you'll receive, even if the funding comes in installments or doesn't arrive right away. For example, let's say a company confirms they'll match an employee's donation in August, but they wait until September to write your organization one check for all matching gifts requested during the third quarter. You'd still recognize the revenue in August when it was pledged.

Exchange Transactions

In contrast to contribution transactions, exchange transactions occur when your nonprofit provides something in return for the funding it receives. While you should show appreciation for every contribution, the difference with exchange transactions is that the funder gives with the expectation of a specific type of reciprocity.

Here are some common types of exchange transactions in a nonprofit context:

- Corporate sponsorships, since businesses are typically promised opportunities for publicity in return for supporting an initiative.

- Membership dues, which are key revenue streams for associations and cultural organizations like museums.

- Branded merchandise sales, product fundraisers, and other purchase-centric revenue-generating activities.

- Crowdfunding and peer-to-peer campaigns where supporters can receive incentives or "perks" for donating at certain levels.

- Sales of event tickets and auction items.

- Fees for services provided—for example, if an animal shelter offered a vaccine clinic for adopted pets, each paid-for vaccine would be an exchange transaction.

Your organization should recognize revenue from exchange transactions when the contributor has received what they were promised. For instance, if you were to sell t-shirts branded to your nonprofit online, you would record the revenue from each purchase when the shirt is shipped to the supporter who ordered it.

Deferred Revenue

Deferred revenue is funding that your organization has received but isn't yet allowed to recognize as income (and therefore can't spend yet). This usually happens with exchange transactions where the supporter pre-pays for a good or service that will be delivered at a later date.

Let's say you work for a nonprofit art museum that offers various paid workshops for community members. You have a four-week landscape painting workshop on the calendar for October, but you open registrations in August to facilitate logistical arrangements for your team. Although participants pay the registration fee when they sign up, your organization can't recognize that revenue until you provide the service you promised in return—the workshop. Therefore, the registration fees are considered deferred revenue until the workshop is finished.

Restricted Funds

Deferred revenue is sometimes confused with restricted funding, since both terms refer to revenue your nonprofit isn't currently allowed to freely spend. However, restricted funds usually come in via contribution transactions rather than exchange transactions, and the restrictions are donor- or funder-imposed regarding how your nonprofit uses the revenue.

There are three categories of restrictions that may apply to your nonprofit's contributions:

- Unrestricted funds have no requirements attached to their use, so your organization can put them toward any area of its budget. Most small-to-mid-sized revenue transactions—both contribution and exchange—fall into this category.

- Permanently restricted funds usually take the form of endowments, a specific type of contribution transaction. Your nonprofit doesn't spend these gifts directly but instead invests them and then uses the interest they generate to fund donor-designated programs or projects.

- Temporarily restricted funds are designated for a specific project or time frame. Once the project is finished or the time expires, any leftover funding is released from restriction. For example, if a major donor contributes $50,000 to a building project and you only end up needing $48,000 of it, the remaining $2,000 becomes unrestricted funding when the project is finished. This category includes most major and planned gifts, grants, and sponsorships (the one commonly restricted exchange transaction).

While you should follow the same transaction-specific procedures for recognizing restricted and unrestricted revenue, make sure to include a separate section in your records for restricted funds to ensure your organization uses them as they're designated.

Conditional Revenue

Conditional revenue refers to situations in which the contributor will only provide funding if specific conditions are met, either internally or externally. In these cases, you'll recognize the revenue when the conditions come to fruition.

Bequests are a common form of nonprofit revenue that is often dependent on an external condition—the donor's passing. Therefore, your organization wouldn't record these until the donor has passed away and their estate has been valued so you know how much you'll receive. By contrast, some grants are dependent on your nonprofit internally fulfilling conditions related to the initiative being funded (more on this later).

Common Revenue Recognition Pain Points (& Their Solutions!)

Nonprofit revenue recognition can be complicated and takes time to learn. Let's dive into a few of the most common pain points nonprofits encounter with revenue recognition and discuss how to work through them.

Grant Revenue Recognition

Grants can be tricky to navigate since different funders have varied requirements for every part of the process, from application to reporting. There are also different procedures for recognizing grant revenue depending on the type of grant a funder offers:

- Unconditional grants are usually provided all at once with no strings attached, so you'll record them as you would most contribution transactions—as soon as you receive the award letter, even if the funding takes additional time to arrive.

- Conditional grants are paid out in installments as your organization meets funder-imposed conditions (for example, they may only agree to fund a community program as long as it has a certain number of participants). Record the first installment of a conditional grant when you receive the award letter and subsequent installments as you receive the funding.

- Reimbursable grants require your nonprofit to spend the money for an initiative up front and keep an itemized list of your expenses so the funder can reimburse you for them. Record these grants when you receive the funding since you likely won't know the exact grant amount until the funder reviews your expense list and makes the payment.

As soon as you identify a grant opportunity for your organization, note its type so you're prepared to recognize the revenue properly if you win it.

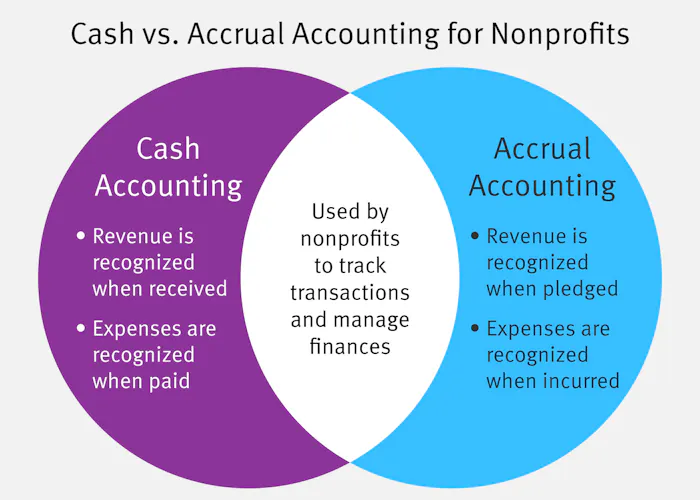

Accounting Methods

Your nonprofit's revenue recognition structure depends on which accounting method you use: cash or accrual basis. Here is a quick overview of these systems:

- Cash accounting systems recognize revenue when it's paid and expenses when they're paid in order to track the flow of cash in and out of your organization.

- Accrual accounting systems recognize revenue when it's pledged and expenses when they're incurred to reflect your nonprofit's financial commitments.

The accrual accounting method is your best bet for effectively managing every aspect of revenue recognition. Although it's more complicated than cash accounting and requires your nonprofit to invest in specialized accounting software rather than simply using a spreadsheet to track transactions, it's worth making the switch to ensure compliance.

In-Kind Donation Management

As mentioned previously, in-kind gifts of goods, services, and non-cash assets are common examples of contribution transactions. Many nonprofits can benefit from them, and these contributions can come from individual donors or corporate sponsors.

However, in-kind donations can be tricky to recognize properly because of a few complex aspects of their recording and reporting procedures, including:

- Net zero gains in cash. In-kind donation values should be recorded as a debit and a credit in your accounting system because they don't cause your organization's cash balance to increase or decrease.

- The potential for multiple transactions. If your nonprofit receives a donated good or non-cash asset and later sells it—such as an auction item or a share of stock—the sale is a separate (usually exchange) transaction from the original contribution.

- To report or not to report value. Your financial statements and tax returns should include the monetary value of in-kind donations among your reported revenue, but your nonprofit isn't legally allowed to state the value of in-kind gifts on donation receipts. Rather, the contributor has to fill it in themselves.

- Valuation procedures. Even before you think about whether to report the fair market value (FMV) of an in-kind donation, you have to figure out what that FMV is, but determining how much a unique or variably priced contribution would be worth if you bought it on the open market can be complicated.

If you need help addressing that last challenge, you've come to the right place! Use the decision tree below to find the right FMV approach for your organization:

Fair Market Value Calculator

Determine the FMV of your in-kind donation

Step 1 of 3

What type of donation is this?

Step 2 of 3

Step 3 of 3

How to Determine FMV

Recordkeeping Reminder: Always document your FMV determination method and sources for tax reporting, GAAP compliance, and potential audits.

Need help recording and reporting in-kind donations?

Work with the nonprofit accountants at Jitasa to make sure every gift is properly valued and recorded.

Request a QuoteTip: Always consult your accountant for specific valuation advice, especially for high-value or complex donations.

The revenue recognition tips above should provide a solid starting point for your nonprofit. However, the best way to overcome the challenges associated with it is to work with a nonprofit accountant (like the experts at Jitasa!) who can use their years of experience and financial expertise to tailor their accounting approach to your organization's unique needs. Your accountant will also be well versed in compliance to ensure your organization can continue to grow and thrive as it brings in even more revenue for its mission.

For more information on recording and reporting nonprofit revenue, check out these resources:

- Grant Management: How to Secure and Track Nonprofit Funding. Dive deeper into every aspect of the grant management cycle, from grantseeking to proposal-writing to reporting.

- Getting Started With Nonprofit Bookkeeping: A Complete Guide. Proper revenue recognition is essential for effective bookkeeping—discover why and how in this guide.

- How to Set up QuickBooks for Nonprofits: The Complete Guide. Explore the best accounting software on the market, QuickBooks Online, and learn how to configure it for your nonprofit's needs.

Work with Jitasa's expert accountants to develop your nonprofit's revenue recognition system.

Request a Quote